That said, for those who are on a cheaper standard variable rate SVR deal, or would move to one at the end of any introductory offer it may pay to simply stay put. With fears of a double-dip recession it is unlikely that central banks will push up interest rates any time soon. However, competitive fixed rates are at present, they are still significantly higher than the 2.

Find out how to invest in recovery with this free guide. Help protect yourself from Identity Fraud with CreditExpert. The best way to transfer money overseas. Get our free weekly Money newsletter. Accessibility links Skip to article Skip to navigation. Wednesday 19 December Telegraph Travel Collection Explore exclusive holidays, tours and cruises. Telegraph International Money Transfer Get the best exchange rates and free expert guidance.

Compare energy prices Find the cheapest gas and electricity prices near you. Free Experian credit score Unlimited access to your credit report and score. I have a joint account, how much is protected? How can I check which bank owns which brand This can be complex, particularly due to the number of mergers and acquisition in recent years.

What about overseas banks? Other economists argue that no matter how much Greece and Portugal drive down their wages, they could never compete with low-cost developing countries such as China or India. Instead weak European countries must shift their economies to higher quality products and services, though this is a long-term process and may not bring immediate relief. Another option would be to implement fiscal devaluation , based on an idea originally developed by John Maynard Keynes in Germany has successfully pushed its economic competitiveness by increasing the value added tax VAT by three percentage points in , and using part of the additional revenues to lower employer's unemployment insurance contribution.

Portugal has taken a similar stance [] and also France appears to follow this suit. According to the report most critical eurozone member countries are in the process of rapid reforms.

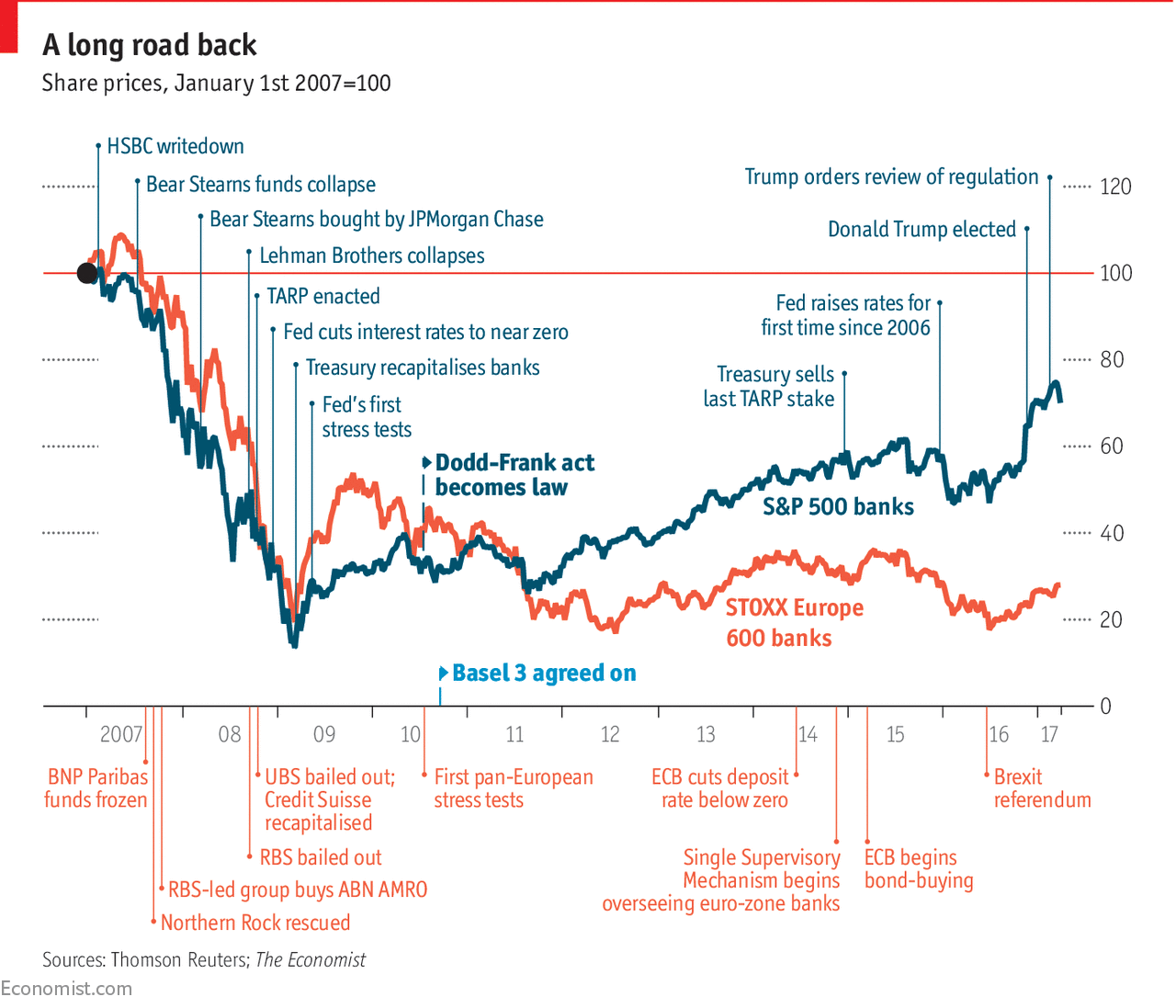

Timeline: The unfolding eurozone crisis

The authors note that "Many of those countries most in need to adjust [ Greece, Ireland and Spain are among the top five reformers and Portugal is ranked seventh among 17 countries included in the report see graph. In its Euro Plus Monitor Report , published in November , the Lisbon Council finds that the eurozone has slightly improved its overall health. With the exception of Greece, all eurozone crisis countries are either close to the point where they have achieved the major adjustment or are likely to get there over the course of Portugal and Italy are expected to progress to the turnaround stage in spring , possibly followed by Spain in autumn, while the fate of Greece continues to hang in the balance.

Overall, the authors suggest that if the eurozone gets through the current acute crisis and stays on the reform path "it could eventually emerge from the crisis as the most dynamic of the major Western economies". The Euro Plus Monitor update from spring notes that the eurozone remains on the right track. According to the authors, almost all vulnerable countries in need of adjustment "are slashing their underlying fiscal deficits and improving their external competitiveness at an impressive speed", for which they expected the eurozone crisis to be over by the end of Regardless of the corrective measures chosen to solve the current predicament, as long as cross border capital flows remain unregulated in the euro area, [] current account imbalances are likely to continue.

A country that runs a large current account or trade deficit i. In other words, a country that imports more than it exports must either decrease its savings reserves or borrow to pay for those imports. Conversely, Germany's large trade surplus net export position means that it must either increase its savings reserves or be a net exporter of capital, lending money to other countries to allow them to buy German goods.

Ben Bernanke warned of the risks of such imbalances in , arguing that a "savings glut" in one country with a trade surplus can drive capital into other countries with trade deficits, artificially lowering interest rates and creating asset bubbles. A country with a large trade surplus would generally see the value of its currency appreciate relative to other currencies, which would reduce the imbalance as the relative price of its exports increases. This currency appreciation occurs as the importing country sells its currency to buy the exporting country's currency used to purchase the goods.

Alternatively, trade imbalances can be reduced if a country encouraged domestic saving by restricting or penalising the flow of capital across borders, or by raising interest rates, although this benefit is likely offset by slowing down the economy and increasing government interest payments.

Either way, many of the countries involved in the crisis are on the euro, so devaluation, individual interest rates, and capital controls are not available. The only solution left to raise a country's level of saving is to reduce budget deficits and to change consumption and savings habits. For example, if a country's citizens saved more instead of consuming imports, this would reduce its trade deficit. On the other hand, export driven countries with a large trade surplus, such as Germany, Austria and the Netherlands would need to shift their economies more towards domestic services and increase wages to support domestic consumption.

Economic evidence indicates the crisis may have more to do with trade deficits which require private borrowing to fund than public debt levels. Economist Paul Krugman wrote in March In its spring economic forecast, the European Commission finds "some evidence that the current-account rebalancing is underpinned by changes in relative prices and competitiveness positions as well as gains in export market shares and expenditure switching in deficit countries".

According to the Euro Plus Monitor Report , the collective current account of Greece, Ireland, Italy, Portugal, and Spain is improving rapidly and is expected to balance by mid Thereafter these countries as a group would no longer need to import capital. Several proposals were made in mid to purchase the debt of distressed European countries such as Spain and Italy. Markus Brunnermeier , [] the economist Graham Bishop, and Daniel Gros were among those advancing proposals. Finding a formula, which was not simply backed by Germany, is central in crafting an acceptable and effective remedy.

In addition, they're going to have to look at how do they achieve growth at the same time as they're carrying out structural reforms that may take two or three or five years to fully accomplish. So countries like Spain and Italy, for example, have embarked on some smart structural reforms that everybody thinks are necessary—everything from tax collection to labour markets to a whole host of different issues.

But they've got to have the time and the space for those steps to succeed. And if they are just cutting and cutting and cutting, and their unemployment rate is going up and up and up, and people are pulling back further from spending money because they're feeling a lot of pressure—ironically, that can actually make it harder for them to carry out some of these reforms over the long term The Economist wrote in June Merkel must do to preserve the single currency. It includes shifting from austerity to a far greater focus on economic growth; complementing the single currency with a banking union with euro-wide deposit insurance, bank oversight and joint means for the recapitalisation or resolution of failing banks ; and embracing a limited form of debt mutualisation to create a joint safe asset and allow peripheral economies the room gradually to reduce their debt burdens.

This is the refrain from Washington, Beijing, London, and indeed most of the capitals of the euro zone. Why hasn't the continent's canniest politician sprung into action? The crisis is pressuring the Euro to move beyond a regulatory state and towards a more federal EU with fiscal powers. Control, including requirements that taxes be raised or budgets cut, would be exercised only when fiscal imbalances developed.

On 6 June , the European Commission adopted a legislative proposal for a harmonised bank recovery and resolution mechanism. The proposed framework sets out the necessary steps and powers to ensure that bank failures across the EU are managed in a way that avoids financial instability. The proposal is part of a new scheme in which banks will be compelled to "bail-in" their creditors whenever they fail, the basic aim being to prevent taxpayer-funded bailouts in the future.

Each institution would also be obliged to set aside at least one per cent of the deposits covered by their national guarantees for a special fund to finance the resolution of banking crisis starting in A growing number of investors and economists say Eurobonds would be the best way of solving a debt crisis, [] though their introduction matched by tight financial and budgetary co-ordination may well require changes in EU treaties.

Using the term "stability bonds", Jose Manuel Barroso insisted that any such plan would have to be matched by tight fiscal surveillance and economic policy coordination as an essential counterpart so as to avoid moral hazard and ensure sustainable public finances. Germany remains largely opposed at least in the short term to a collective takeover of the debt of states that have run excessive budget deficits and borrowed excessively over the past years. ESBies could be issued by public or private-sector entities and would "weaken the diabolic loop and its diffusion across countries".

It requires "no significant change in treaties or legislation. In the idea was picked up by the European Central Bank. The European Commission has also shown interest and plans to include ESBies in a future white paper dealing with the aftermath of the financial crisis. On 20 October , the Austrian Institute of Economic Research published an article that suggests transforming the EFSF into a European Monetary Fund EMF , which could provide governments with fixed interest rate Eurobonds at a rate slightly below medium-term economic growth in nominal terms. These bonds would not be tradable but could be held by investors with the EMF and liquidated at any time.

To ensure fiscal discipline despite lack of market pressure, the EMF would operate according to strict rules, providing funds only to countries that meet fiscal and macroeconomic criteria. Governments lacking sound financial policies would be forced to rely on traditional national governmental bonds with less favourable market rates.

The econometric analysis suggests that "If the short-term and long- term interest rates in the euro area were stabilised at 1. At the same time, sovereign debt levels would be significantly lower with, e. Furthermore, banks would no longer be able to benefit unduly from intermediary profits by borrowing from the ECB at low rates and investing in government bonds at high rates.

The Boston Consulting Group BCG adds that if the overall debt load continues to grow faster than the economy, then large-scale debt restructuring becomes inevitable. The authors admit that such programmes would be "drastic", "unpopular" and "require broad political coordination and leadership" but they maintain that the longer politicians and central bankers wait, the more necessary such a step will be. Thomas Piketty , French economist and author of the bestselling book Capital in the Twenty-First Century regards taxes on capital as a more favorable option than austerity inefficient and unjust and inflation only affects cash but neither real estates nor business capital.

According to his analysis, a flat tax of 15 percent on private wealth would provide the state with nearly a year's worth national income, which would allow for immediate reimbursement of the entire public debt. Instead of a one-time write-off, German economist Harald Spehl has called for a year debt-reduction plan, similar to the one Germany used after World War II to share the burden of reconstruction and development.

According to this agreement, West Germany had to make repayments only when it was running a trade surplus, that is "when it had earned the money to pay up, rather than having to borrow more, or dip into its foreign currency reserves. The European bailouts are largely about shifting exposure from banks and others, who otherwise are lined up for losses on the sovereign debt they have piled up, onto European taxpayers.

First, the "no bail-out" clause Article TFEU ensures that the responsibility for repaying public debt remains national and prevents risk premiums caused by unsound fiscal policies from spilling over to partner countries. The clause thus encourages prudent fiscal policies at the national level. The European Central Bank 's purchase of distressed country bonds can be viewed as violating the prohibition of monetary financing of budget deficits Article TFEU. Articles and were meant to create disincentives for EU member states to run excessive deficits and state debt, and prevent the moral hazard of over-spending and lending in good times.

BBC News Navigation

They were also meant to protect the taxpayers of the other more prudent member states. By issuing bail-out aid guaranteed by prudent eurozone taxpayers to rule-breaking eurozone countries such as Greece, the EU and eurozone countries also encourage moral hazard in the future. The EU treaties contain so called convergence criteria , specified in the protocols of the Treaties of the European Union. For eurozone members there is the Stability and Growth Pact , which contains the same requirements for budget deficit and debt limitation but with a much stricter regime.

In the past, many European countries have substantially exceeded these criteria over a long period of time. According to a study by economists at St Gallen University credit rating agencies have fuelled rising euro zone indebtedness by issuing more severe downgrades since the sovereign debt crisis unfolded in The authors concluded that rating agencies were not consistent in their judgments, on average rating Portugal, Ireland, and Greece 2. Germany, Finland and Luxembourg. European policy makers have criticised ratings agencies for acting politically, accusing the Big Three of bias towards European assets and fuelling speculation.

France too has shown its anger at its downgrade. Similar comments were made by high-ranking politicians in Germany. Michael Fuchs , deputy leader of the leading Christian Democrats , said: Why doesn't it act on the highly indebted United States or highly indebted Britain? Credit rating agencies were also accused of bullying politicians by systematically downgrading eurozone countries just before important European Council meetings.

As one EU source put it: It is strange that we have so many downgrades in the weeks of summits.

In essence, this forced European banks and more importantly the European Central Bank , e. Due to the failures of the ratings agencies, European regulators obtained new powers to supervise ratings agencies. Germany's foreign minister Guido Westerwelle called for an "independent" European ratings agency, which could avoid the conflicts of interest that he claimed US-based agencies faced. On 30 January , the company said it was already collecting funds from financial institutions and business intelligence agencies to set up an independent non-profit ratings agency by mid, which could provide its first country ratings by the end of the year.

But attempts to regulate credit rating agencies more strictly in the wake of the eurozone crisis have been rather unsuccessful. Some in the Greek, Spanish, and French press and elsewhere spread conspiracy theories that claimed that the U. The Economist rebutted these "Anglo-Saxon conspiracy" claims, writing that although American and British traders overestimated the weakness of southern European public finances and the probability of the breakup of the eurozone breakup, these sentiments were an ordinary market panic, rather than some deliberate plot.

Greek Prime Minister Papandreou is quoted as saying that there was no question of Greece leaving the euro and suggested that the crisis was politically as well as financially motivated. Both the Spanish and Greek Prime Ministers have accused financial speculators and hedge funds of worsening the crisis by short selling euros. Goldman Sachs and other banks faced an inquiry by the Federal Reserve over their derivatives arrangements with Greece. The Guardian reported that "Goldman was reportedly the most heavily involved of a dozen or so Wall Street banks" that assisted the Greek government in the early s "to structure complex derivatives deals early in the decade and 'borrow' billions of dollars in exchange rate swaps, which did not officially count as debt under eurozone rules.

In response to accusations that speculators were worsening the problem, some markets banned naked short selling for a few months. Some economists, mostly from outside Europe and associated with Modern Monetary Theory and other post-Keynesian schools, condemned the design of the euro currency system from the beginning because it ceded national monetary and economic sovereignty but lacked a central fiscal authority. When faced with economic problems, they maintained, "Without such an institution, EMU would prevent effective action by individual countries and put nothing in its place.

Ricci of the IMF, contend that the eurozone does not fulfil the necessary criteria for an optimum currency area , though it is moving in that direction. As the debt crisis expanded beyond Greece, these economists continued to advocate, albeit more forcefully, the disbandment of the eurozone. If this was not immediately feasible, they recommended that Greece and the other debtor nations unilaterally leave the eurozone, default on their debts, regain their fiscal sovereignty, and re-adopt national currencies.

The likely substantial fall in the euro against a newly reconstituted Deutsche Mark would give a "huge boost" to its members' competitiveness.

Iceland, not part of the EU, is regarded as one of Europe's recovery success stories. Labour concessions, a minimal reliance on public debt, and tax reform helped to further a pro-growth policy. The Wall Street Journal added that without the German-led bloc, a residual euro would have the flexibility to keep interest rates low [] and engage in quantitative easing or fiscal stimulus in support of a job-targeting economic policy [] instead of inflation targeting in the current configuration.

There is opposition in this view. The national exits are expected to be an expensive proposition. The breakdown of the currency would lead to insolvency of several euro zone countries, a breakdown in intrazone payments. Having instability and the public debt issue still not solved, the contagion effects and instability would spread into the system. According to Steven Erlanger from The New York Times, a "Greek departure is likely to be seen as the beginning of the end for the whole euro zone project, a major accomplishment, whatever its faults, in the post-War construction of a Europe "whole and at peace".

The challenges to the speculation about the break-up or salvage of the eurozone is rooted in its innate nature that the break-up or salvage of eurozone is not only an economic decision but also a critical political decision followed by complicated ramifications that "If Berlin pays the bills and tells the rest of Europe how to behave, it risks fostering destructive nationalist resentment against Germany and The Economist provides a somewhat modified approach to saving the euro in that "a limited version of federalisation could be less miserable solution than break-up of the euro".

In order for overindebted countries to stabilise the dwindling euro and economy, the overindebted countries require "access to money and for banks to have a "safe" euro-wide class of assets that is not tied to the fortunes of one country" which could be obtained by "narrower Eurobond that mutualises a limited amount of debt for a limited amount of time". Instead of the break-up and issuing new national governments bonds by individual euro-zone governments, "everybody, from Germany debt: Each country would pledge a specified tax such as a VAT surcharge to provide the cash.

He argues that to save the Euro long-term structural changes are essential in addition to the immediate steps needed to arrest the crisis. The changes he recommends include even greater economic integration of the European Union. Following the formation of the Treasury, the European Council could then authorise the ECB to "step into the breach", with risks to the ECB's solvency being indemnified. In particular, he cautions, Germans will be wary of any such move, not least because many continue to believe that they have a choice between saving the Euro and abandoning it.

Soros writes that a collapse of the European Union would precipitate an uncontrollable financial meltdown and thus "the only way" to avert "another Great Depression" is the formation of a European Treasury.

- European debt crisis - Wikipedia.

- SuperFit SuperFast Nutrition: The Busy Persons Guide To Increasing Energy and Losing Weight.

- To These Things You Must Return - Part One: Karl Butler and the Original Manatoc (To These Things You Must Return - A History of the Manatoc Scout Reservation Book 1).

- Determinants of the Death Penalty: A Comparative Study of the World (Routledge Research in Comparative Politics).

In , members of the European Union signed an agreement known as the Maastricht Treaty , under which they pledged to limit their deficit spending and debt levels. Some EU member states, including Greece and Italy, were able to circumvent these rules and mask their deficit and debt levels through the use of complex currency and credit derivatives structures.

This added a new dimension in the world financial turmoil, as the issues of " creative accounting " and manipulation of statistics by several nations came into focus, potentially undermining investor confidence. The focus has naturally remained on Greece due to its debt crisis.

There have been reports about manipulated statistics by EU and other nations aiming, as was the case for Greece, to mask the sizes of public debts and deficits. These have included analyses of examples in several countries [] [] [] [] [] the United Kingdom, [] [] [] [] [] Spain, [] the United States, [] [] [] and even Germany. After extensive negotiations to implement a collateral structure open to all eurozone countries, on 4 October , a modified escrow collateral agreement was reached. The expectation is that only Finland will utilise it, due, in part, to a requirement to contribute initial capital to European Stability Mechanism in one instalment instead of five instalments over time.

Finland, as one of the strongest AAA countries, can raise the required capital with relative ease. At the beginning of October, Slovakia and Netherlands were the last countries to vote on the EFSF expansion , which was the immediate issue behind the collateral discussion, with a mid-October vote. Finland's recommendation to the crisis countries is to issue asset-backed securities to cover the immediate need, a tactic successfully used in Finland's early s recession , [] in addition to spending cuts and bad banking.

The handling of the crisis has led to the premature end of several European national governments and influenced the outcome of many elections:. This section is very long. You can click here to skip it. From Wikipedia, the free encyclopedia.

Timeline: The unfolding eurozone crisis - BBC News

Causes of the European debt crisis. Public debt in , Source: European Commission [14] Legend: Post Irish economic downturn. Policy reactions to the eurozone crisis. European Financial Stability Facility. European Financial Stabilisation Mechanism. Economic reforms and recovery proposals regarding the Eurozone crisis. Proposed long-term solutions for the European sovereign-debt crisis. Controversies surrounding the Eurozone crisis. Consolidated version of the Treaty on the Functioning of the European Union. Greek withdrawal from the eurozone. Retrieved 22 July Italy hit with rating downgrade".

Retrieved 20 September Retrieved 7 July Archived from the original on 15 June Retrieved 30 January Schwartz; Tom Kuntz 22 October A Spectators Guide to the Euro Crisis". The New York Times. Retrieved 14 May Retrieved 28 April Retrieved 22 June Retrieved 6 July Nelson and Darek E. Mix "The Eurozone Crisis: Retrieved 6 January Inaccuracies and Evidence of Manipulation". Retrieved 14 October Brookings Papers on Economic Activity, Spring Retrieved 15 April Retrieved 8 December Retrieved 30 July Archived from the original on 18 October Retrieved 6 September Retrieved 13 November Retrieved 7 November Retrieved 18 May Myths, Popular Notions and Implications".

Archived from the original on 25 May Archived from the original on 2 February Retrieved 6 May The Observer at Boston College. Archived from the original on 12 September Retrieved 5 May Archived from the original on 30 December Retrieved 30 December Retrieved 29 December Retrieved 1 February Retrieved 13 February Archived from the original PDF on 17 June Retrieved 9 March Retrieved 2 March Industrial production down by 1.

Archived from the original PDF on 16 February Retrieved 5 March UK credit rating under threat amid Moody's downgrade blitz". Retrieved 14 February Retrieved 9 February Retrieved 16 February Retrieved 4 November Euro area unemployment rate at Archived from the original PDF on 1 March Retrieved 27 June Archived from the original PDF on 9 February Greeks can't take any more punishment".

International Business and Political Economy. Retrieved 24 September Retrieved 16 May Retrieved 23 January Retrieved 3 August Retrieved 3 March How the Greek debt puzzle was solved". Retrieved 29 February Retrieved 13 March Retrieved 18 April Retrieved 21 February Retrieved 27 March Retrieved 20 January Retrieved 12 March Lancaster University Management School.

Archived from the original PDF on 25 November Retrieved 2 April Retrieved 5 April Retrieved 9 May Retrieved 28 January The Germans might have preferred a victory by the left in Athens". Retrieved 17 May Having suffered the worst financial and economic crisis of the last 80 years, Europe took decisive action to improve its public finances, push through deep reforms, and establish new institutions to manage and prevent crises better.

The changes are structural, long-lasting and make Europe more competitive. Europe is stronger, better equipped and in the midst of ambitious new financial and economic initiatives. The global crisis hit Europe twice. The first strike came from abroad in In the United States, markets had ignored credit risk in subprime mortgage markets. A lack of financial supervision allowed opaque financial instruments to flourish, aggravating the problem.

As a result, the U. European banks suffered in the fallout. Two years later, a second crisis erupted in the euro area. Years of unsustainable government policies had caused deficits and debt burdens to mushroom and bloated pre-crisis wages and housing prices. As the situation worsened, Europe took courageous decisions to put the continent back on firm footing.

First, crisis-hit countries like Ireland and Spain pushed through badly needed reforms, improving public finances and increasing competitiveness. Second, EU economic governance was strengthened. These institutions were a great success: Importantly, no European taxpayer money was spent on the rescue programmes.

This approach produces budget savings for programme countries, particularly Greece, which would pay much more if it were to tap capital markets independently.

Accessibility links

The ECB expanded its balance sheet like the FED, Bank of Japan and Bank of England, provided unlimited liquidity for banks, started a bond purchasing programme to avoid low inflation, which also made it easier for banks to lend and boost investor sentiment. The euro weakened which helped to increase exports. Finally, the Banking Union was established: The Single Supervisory Mechanism is the centrepiece of this initiative; it oversees the largest euro area banks. The results are impressive figure 2.

The crisis-hit countries implemented radical reforms. They did so by improving their public finances, reducing deficits, and cutting labour costs to make themselves more competitive. And finally, some of the crisis countries are becoming growth leaders. In , Ireland hit a record high 6. These are extraordinary achievements. During the crisis, Europe picked up the pace of policy reform and integration with three big initiatives that merit close attention.