You know your modified adjusted gross income. You know your net investment income. To calculate the net investment income tax, first subtract the threshold figure shown above for your filing status from your MAGI. Then compare the result with your net investment income. Multiply the lower of the two figures by 3. The instructions for IRS Form provide an overview of the rules that apply and can be a good source of additional information.

What income thresholds apply? The net investment income tax applies only if your modified adjusted gross income exceeds the following thresholds: What is net investment income? How is the tax calculated? How is it reported? If you reinvest your Treasury bill at its maturity in a new Treasury bill, note, or bond, you will receive payment for the difference between the proceeds of the maturing bill par amount less any tax withheld and the purchase price of the new Treasury security. However, you must report the full amount of the interest income on each of your Treasury bills at the time it reaches maturity.

Treasury notes have maturity periods of more than 1 year, ranging up to 10 years. Maturity periods for Treasury bonds are longer than 10 years. Generally, you report this interest for the year paid. When the notes or bonds mature, you can redeem these securities for face value or use the proceeds from the maturing note or bond to reinvest in another note or bond of the same type and term. If you do nothing, the proceeds from the maturing note or bond will be deposited in your bank account.

Treasury notes and bonds are sold by auction. Two types of bids are accepted: If you make a competitive bid and a determination is made that the purchase price is less than the face value, you will receive a refund for the difference between the purchase price and the face value. This amount is considered original issue discount. See De minimis OID , later. If the purchase price is determined to be more than the face amount, the difference is a premium.

See Bond Premium Amortization in chapter 3. Or, on the Internet, visit www. These securities pay interest twice a year at a fixed rate, based on a principal amount adjusted to take into account inflation and deflation. For the tax treatment of these securities, see Inflation-Indexed Debt Instruments , later. For information on the retirement, sale, or redemption of U. Also see Nontaxable Trades in chapter 4 for information about trading U.

Treasury obligations for certain other designated issues. If you sell a bond between interest payment dates, part of the sales price represents interest accrued to the date of sale. You must report that part of the sales price as interest income for the year of sale. If you buy a bond between interest payment dates, part of the purchase price represents interest accrued before the date of purchase.

When that interest is paid to you, treat it as a return of your capital investment, rather than interest income, by reducing your basis in the bond. See Accrued interest on bonds , later in this chapter, for information on reporting the payment. Life insurance proceeds paid to you as the beneficiary of the insured person are usually not taxable. But if you receive the proceeds in installments, you must usually report part of each installment payment as interest income. If you leave life insurance proceeds on deposit with an insurance company under an agreement to pay interest only, the interest paid to you is taxable.

If you buy an annuity with life insurance proceeds, the annuity payments you receive are taxed as pension and annuity income from a nonqualified plan, not as interest income. Interest you receive on an obligation issued by a state or local government is generally not taxable. The issuer should be able to tell you whether the interest is taxable. The issuer should also give you a periodic or year-end statement showing the tax treatment of the obligation.

If you invested in the obligation through a trust, a fund, or other organization, that organization should give you this information. Even if interest on the obligation is not subject to income tax, you may have to report a capital gain or loss when you sell it.

- Pray for Me: The Power in Praying for Others.

- Understanding Your Taxes: Social Security, Retirement Instruments, and Capital Gains.

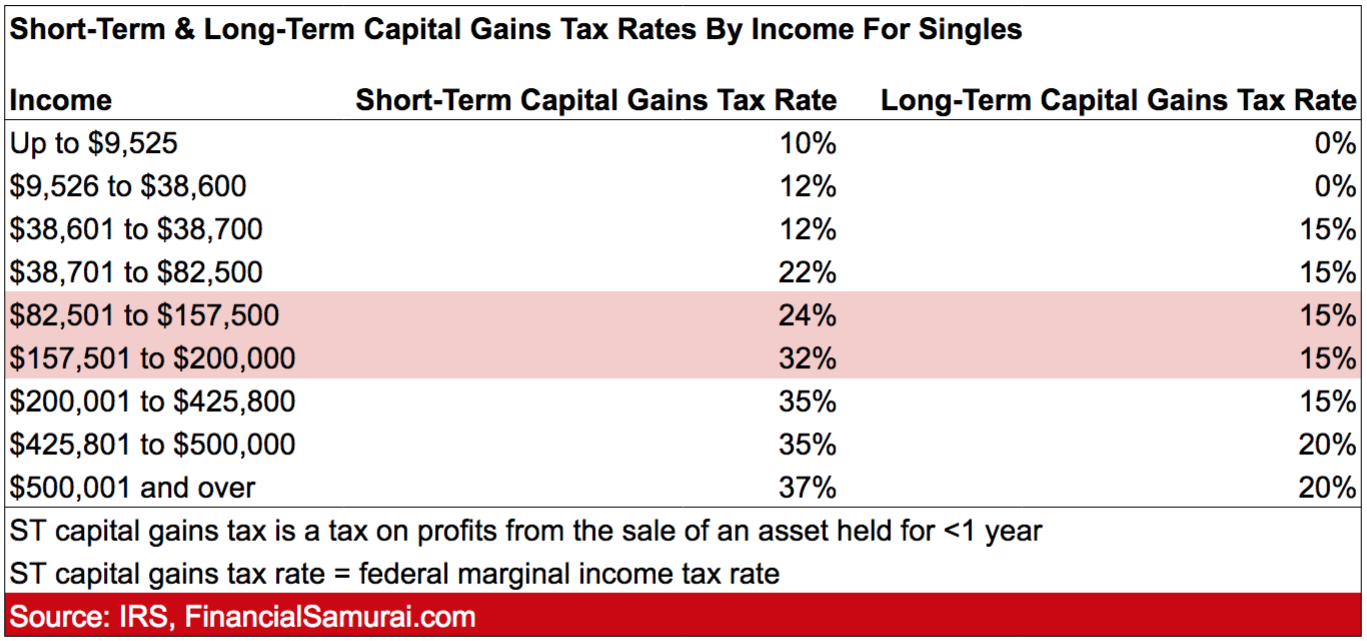

- Understanding the Net Investment Income Tax;

Estate, gift, or generation-skipping tax may apply to other dispositions of the obligation. Interest on a bond used to finance government operations generally is not taxable if the bond is issued by a state, the District of Columbia, a U. There are other requirements for tax-exempt bonds.

Contact the issuing state or local government agency or see sections and through of the Internal Revenue Code and the related regulations. Obligations that are not bonds. Interest on a state or local government obligation may be tax exempt even if the obligation is not a bond.

For example, interest on a debt evidenced only by an ordinary written agreement of purchase and sale may be tax exempt. Also, interest paid by an insurer on default by the state or political subdivision may be tax exempt. A bond issued after June 30, , generally must be in registered form for the interest to be tax exempt. Bonds issued after by an Indian tribal government including tribal economic development bonds issued after February 17, are treated as issued by a state.

Interest on these bonds is generally tax exempt if the bonds are part of an issue of which substantially all proceeds are to be used in the exercise of any essential government function. However, the essential government function requirement does not apply to tribal economic development bonds issued after February 17, , for tax-exempt treatment. Interest on private activity bonds other than certain bonds for tribal manufacturing facilities is taxable. Original issue discount OID on tax-exempt state or local government bonds is treated as tax-exempt interest.

For information on the treatment of OID when you dispose of a tax-exempt bond, see Tax-exempt state and local government bonds , later. For special rules that apply to stripped tax-exempt obligations, see Stripped Bonds and Coupons , later. If you must file a tax return, you are required to show any tax-exempt interest you received on your return. This is an information reporting requirement only. It does not change tax-exempt interest to taxable interest.

See Reporting tax-exempt interest , later in this chapter. Interest on federally guaranteed state or local obligations issued after is generally taxable. This rule does not apply to interest on obligations guaranteed by the following U. Federal home loan banks. The guarantee must be made after July 30, , in connection with the original bond issue during the period beginning on July 30, , and ending on December 31, or a renewal or extension of a guarantee so made and the bank must meet safety and soundness requirements.

Tax credit bonds generally do not pay interest. Instead, the bondholder is allowed an annual tax credit. The credit compensates the holder for lending money to the issuer and functions as interest paid on the bond. Use Form , Credit to Holders of Tax Credit Bonds, to claim the credit for the following tax credit bonds and to figure the amount of the credit to report as interest income. The proceeds of these bonds are used to finance mortgage loans for homebuyers. Generally, interest on state or local government home mortgage bonds issued after April 24, , is taxable unless the bonds are qualified mortgage bonds or qualified veterans' mortgage bonds.

Interest on arbitrage bonds issued by state or local governments after October 9, , is taxable. An arbitrage bond is a bond any portion of the proceeds of which is expected to be used to buy or to replace funds used to buy higher yielding investments. A bond is treated as an arbitrage bond if the issuer intentionally uses any part of the proceeds of the issue in this manner. Interest on a private activity bond that is not a qualified bond defined below is taxable. Generally, a private activity bond is part of a state or local government bond issue that meets both the following requirements.

Secured by an interest in property to be used for a private business use or payments for this property , or. Derived from payments for property or borrowed money used for a private business use. Interest on a private activity bond that is a qualified bond is tax exempt.

A qualified bond is an exempt-facility bond including an enterprise zone facility bond, a New York Liberty bond, a Midwestern disaster area bond, a Hurricane Ike disaster area bond, a Gulf Opportunity Zone bond treated as an exempt-facility bond, or any recovery zone facility bond issued after February 17, , and before January 1, , qualified student loan bond, qualified small issue bond including a tribal manufacturing facility bond , qualified redevelopment bond, qualified mortgage bond including a Gulf Opportunity Zone bond, a Midwestern disaster area bond, or a Hurricane Ike disaster area bond treated as a qualified mortgage bond , qualified veterans' mortgage bond, or qualified c 3 bond a bond issued for the benefit of certain tax-exempt organizations.

Interest you receive on these tax-exempt bonds, if issued after August 7, , generally is a "tax preference item" and may be subject to the alternative minimum tax. See Form and its instructions for more information. The interest on the following bonds is not a tax preference item and is not subject to the alternative minimum tax.

The interest on any qualified bond issued in or is not a tax preference item and is not subject to the alternative minimum tax. For this purpose, a refunding bond whether a current or advanced refunding is treated as issued on the date the refunded bond was issued or on the date the original bond was issued in the case of a series of refundings. However, this rule does not apply to any refunding bond issued to refund any qualified bond issued during through or after A portion of the interest on specified private activity bonds issued after December 31, , may be a tax preference item subject to the alternative minimum tax.

The tax preference status will apply to the portion of the interest that remains after reducing it by deductions that would be allowed if the interest were taxable. Interest on certain private activity bonds issued by a state or local government to finance a facility used in an empowerment zone or enterprise community is tax exempt. New York Liberty bonds are bonds issued after March 9, , to finance the construction and rehabilitation of real property in the designated "Liberty Zone" of New York City.

Interest on these bonds issued before is tax exempt. Market discount on a tax-exempt bond is not tax-exempt. If you bought the bond after April 30, , you can choose to accrue the market discount over the period you own the bond and include it in your income currently as taxable interest. See Market Discount Bonds , later. If you do not make that choice, or if you bought the bond before May 1, , any gain from market discount is taxable when you dispose of the bond. For more information on the treatment of market discount when you dispose of a tax-exempt bond, see Discounted Debt Instruments , later.

A debt instrument, such as a bond, note, debenture, or other evidence of indebtedness, that bears no interest or bears interest at a lower than current market rate will usually be issued at less than its face amount. This discount is, in effect, additional interest income.

The following are some types of discounted debt instruments. The discount on these instruments except municipal bonds is taxable in most instances. The discount on municipal bonds generally is not taxable but see State or Local Government Obligations , earlier, for exceptions. OID is a form of interest. You generally include OID in your income as it accrues over the term of the debt instrument, whether or not you receive any payments from the issuer.

A debt instrument generally has OID when the instrument is issued for a price that is less than its stated redemption price at maturity. OID is the difference between the stated redemption price at maturity and the issue price. All debt instruments that pay no interest before maturity are presumed to be issued at a discount.

Zero coupon bonds are one example of these instruments. The OID accrual rules generally do not apply to short-term obligations those with a fixed maturity date of 1 year or less from date of issue. This small discount is known as "de minimis" OID. In the case of a debt instrument providing for more than one stated principal payment an installment obligation , the "de minimis" formula described above is modified. See Regulations section 1. If you buy a debt instrument with de minimis OID at a premium, the discount is not includible in income.

If you buy a debt instrument with de minimis OID at a discount, the discount is reported under the market discount rules. See Market Discount Bonds , later in this chapter. The OID rules discussed here do not apply to the following debt instruments. However, see Stripped tax-exempt obligations , later. Short-term debt instruments those with a fixed maturity date of not more than 1 year from the date of issue.

Avoiding any federal tax is not one of the principal purposes of the loan. It also will show, in box 2, the stated interest you must include in your income. Box 8 shows OID on a U. Treasury obligation for the part of the year you owned it and is not included in box 1. Box 10 shows bond premium amortization. Do not file your copy with your return. Keep it for your records.

In most cases, you must report the entire amount in boxes 1, 2, and 8 of Form OID as interest income. If you receive a Form OID that includes amounts belonging to another person, see Nominee distributions , later. You bought the debt instrument after its original issue and paid a premium or an acquisition premium. The debt instrument is a stripped bond or a stripped coupon including certain zero coupon instruments.

See Figuring OID , later in this chapter. You bought a debt instrument at a premium if its adjusted basis immediately after purchase was greater than the total of all amounts payable on the instrument after the purchase date, other than qualified stated interest. In general, this is stated interest unconditionally payable in cash or property other than debt instruments of the issuer at least annually at a fixed rate.

You bought a debt instrument at an acquisition premium if both the following are true. The instrument's adjusted basis immediately after purchase including purchase at original issue was greater than its adjusted issue price. This is the issue price plus the OID previously accrued, minus any payment previously made on the instrument other than qualified stated interest.

Acquisition premium reduces the amount of OID includible in your income. If you disposed of a debt instrument or acquired it from another holder during the year, see Bonds Sold Between Interest Dates , earlier, for information about the treatment of periodic interest that may be shown in box 2 of Form OID for that instrument. Debt instruments issued after May 27, after July 1, , if a government instrument , and before If you hold these debt instruments as capital assets, you must include a part of the discount in your gross income each year that you own the instruments.

Your basis in the instrument is increased by the amount of OID you include in your gross income. For these debt instruments, you report the total OID that applies each year regardless of whether you hold that debt instrument as a capital asset. If you buy a CD with a maturity of more than 1 year, you must include in income each year a part of the total interest due and report it in the same manner as other OID.

This also applies to similar deposit arrangements with banks, building and loan associations, etc. CDs issued after generally must be in registered form. Bearer CDs are CDs not in registered form. They are not issued in the depositor's name and are transferable from one individual to another. This is an arrangement with a fixed maturity date in which you make deposits on a schedule arranged between you and your bank.

But there is no actual or constructive receipt of interest until the fixed maturity date is reached. You must include a part of the interest in your income as OID each year. Each year the bank must give you a Form OID to show you the amount you must include in your income for the year. If, before the maturity date, you redeem a deferred interest account for less than its stated redemption price at maturity, you can deduct OID that you previously included in income but did not receive. If you renew a CD at maturity, it is treated as a redemption and a purchase of a new certificate.

This is true regardless of the terms of renewal. These certificates are subject to the OID rules. They are a form of endowment contracts issued by insurance or investment companies for either a lump-sum payment or periodic payments, with the face amount becoming payable on the maturity date of the certificate. In general, the difference between the face amount and the amount you paid for the contract is OID. You must include a part of the OID in your income over the term of the certificate.

The issuer must give you a statement on Form OID indicating the amount you must include in your income each year. If you hold an inflation-indexed debt instrument other than a Series I U. In general, an inflation-indexed debt instrument is a debt instrument on which the payments are adjusted for inflation and deflation such as Treasury Inflation-Protected Securities.

You should receive Form OID from the payer showing the amount you must report as OID and any qualified stated interest paid to you during the year. For more information, see Pub. If you strip one or more coupons from a bond and sell the bond or the coupons, the bond and coupons are treated as separate debt instruments issued with OID. The holder of a stripped bond has the right to receive the principal redemption price payment.

The holder of a stripped coupon has the right to receive interest on the bond. Instruments backed by U. Treasury securities that represent ownership interests in those securities, such as obligations backed by U. Treasury bonds offered primarily by brokerage firms. If you strip coupons from a bond and sell the bond or coupons, include in income the interest that accrued while you held the bond before the date of sale, to the extent you did not previously include this interest in your income. For an obligation acquired after October 22, , you must also include the market discount that accrued before the date of sale of the stripped bond or coupon to the extent you did not previously include this discount in your income.

Add the interest and market discount that you include in income to the basis of the bond and coupons. Allocate this adjusted basis between the items you keep and the items you sell, based on the fair market value of the items. The difference between the sale price of the bond or coupon and the allocated basis of the bond or coupon is your gain or loss from the sale. Treat any item you keep as an OID bond originally issued and bought by you on the sale date of the other items. If you keep the bond, treat the amount of the redemption price of the bond that is more than the basis of the bond as OID.

If you keep the coupons, treat the amount payable on the coupons that is more than the basis of the coupons as OID. If you buy a stripped bond or stripped coupon, treat it as if it were originally issued on the date you buy it. If you buy a stripped bond, treat as OID any excess of the stated redemption price at maturity over your purchase price. If you buy a stripped coupon, treat as OID any excess of the amount payable on the due date of the coupon over your purchase price. The rules for figuring OID on stripped bonds and stripped coupons depend on the date the debt instruments were purchased, not the date issued.

OID on stripped inflation-indexed debt instruments is figured under the discount bond method. This method is described in Regulations section 1. You do not have to pay tax on OID on any stripped tax-exempt bond or coupon you bought before June 11, However, if you acquired it after October 22, , you must accrue OID on it to determine its basis when you dispose of it. See Original issue discount OID on debt instruments , later. You may have to pay tax on part of the OID on stripped tax-exempt bonds or coupons that you bought after June 10, Market discount arises when the value of a debt obligation decreases after its issue date.

Generally, this is due to an increase in interest rates. If you buy a bond on the secondary market, it may have market discount. When you buy a market discount bond, you can choose to accrue the market discount over the period you own the bond and include it in your income currently as interest income. If you do not make this choice, the following rules generally apply. You must treat any gain when you dispose of the bond as ordinary interest income, up to the amount of the accrued market discount. See Discounted Debt Instruments , later. You must treat any partial payment of principal on the bond as ordinary interest income, up to the amount of the accrued market discount.

See Partial principal payments , later in this discussion. If you borrow money to buy or carry the bond, your deduction for interest paid on the debt is limited. See Limit on interest deduction for market discount bonds , later. Market discount is the amount of the stated redemption price of a bond at maturity that is more than your basis in the bond immediately after you acquire it. If a market discount bond also has OID, the market discount is the sum of the bond's issue price and the total OID includible in the gross income of all holders for a tax-exempt bond, the total OID that accrued before you acquired the bond, reduced by your basis in the bond immediately after you acquired it.

Generally, a bond you acquired at original issue is not a market discount bond. If your adjusted basis in a bond is determined by reference to the adjusted basis of another person who acquired the bond at original issue, you are also considered to have acquired it at original issue. A bond you acquired at original issue can be a market discount bond if either of the following is true.

The bond is issued in exchange for a market discount bond under a plan of reorganization. This does not apply if the bond is issued in exchange for a market discount bond issued before July 19, , and the terms and interest rates of both bonds are the same. Treat the market discount as accruing in equal daily installments during the period you hold the bond.

Figure the daily installments by dividing the market discount by the number of days after the date you acquired the bond, up to and including its maturity date. Multiply the daily installments by the number of days you held the bond to figure your accrued market discount. Instead of using the ratable accrual method, you can choose to figure the accrued discount using a constant interest rate the constant yield method. Make this choice by attaching to your timely filed return a statement identifying the bond and stating that you are making a constant interest rate election.

The choice takes effect on the date you acquired the bond. If you choose to use this method for any bond, you cannot change your choice for that bond. For information about using the constant yield method, see Constant yield method under Debt Instruments Issued After in Pub. To use this method to figure market discount instead of OID , treat the bond as having been issued on the date you acquired it. Treat the amount of your basis immediately after you acquired the bond as the issue price and apply the formula shown in Pub.

You can make this choice if you have not revoked a prior choice to include market discount in income currently within the last 5 calendar years. Make the choice by attaching to your timely filed return a statement in which you: State that you have included market discount in your gross income for the year under section b of the Internal Revenue Code, and. Describe the method you used to figure the accrued market discount for the year.

Once you make this choice, it will apply to all market discount bonds you acquire during the tax year and in later tax years. You cannot revoke your choice without the consent of the IRS. For information on how to revoke your choice, see section 30 of Revenue Procedure in Internal Revenue Bulletin You can find this revenue procedure at www.

If you make that election, you must use the constant yield method. You increase the basis of your bonds by the amount of market discount you include in your income. If you receive a partial payment of principal on a market discount bond you acquired after October 22, , and you did not choose to include the discount in income currently, you must treat the payment as ordinary interest income up to the amount of the bond's accrued market discount. Reduce the amount of accrued market discount reportable as interest at disposition by that amount. There are three methods you can use to figure accrued market discount for this purpose.

In proportion to the amount of stated interest paid in the accrual period, if the debt instrument has no OID. Under method 2 above, figure accrued market discount for a period by multiplying the total remaining market discount by a fraction. The numerator top part of the fraction is the OID for the period, and the denominator bottom part is the total remaining OID at the beginning of the period. Under method 3 above, figure accrued market discount for a period by multiplying the total remaining market discount by a fraction. The numerator is the stated interest paid in the accrual period, and the denominator is the total stated interest remaining to be paid at the beginning of the accrual period.

When you buy a short-term obligation one with a fixed maturity date of 1 year or less from the date of issue , other than a tax-exempt obligation, you can generally choose to include any discount and interest payable on the obligation in income currently. You must treat any gain when you sell, exchange, or redeem the obligation as ordinary income, up to the amount of the ratable share of the discount. If you borrow money to buy or carry the obligation, your deduction for interest paid on the debt is limited. See Limit on interest deduction for short-term obligations , later.

You must include any discount or interest in current income as it accrues for any short-term obligation other than a tax-exempt obligation that is: Held primarily for sale to customers in the ordinary course of your trade or business;. A stripped bond or stripped coupon held by the person who stripped the bond or coupon or by any other person whose basis in the obligation is determined by reference to the basis in the hands of the person who stripped the bond or coupon. Increase the basis of your obligation by the amount of discount you include in income currently.

Figure the accrued discount by using either the ratable accrual method or the constant yield method discussed in Accrued market discount , earlier. For an obligation described above that is a short-term government obligation, the amount you include in your income for the current year is the accrued acquisition discount, if any, plus any other accrued interest payable on the obligation. The acquisition discount is the stated redemption price at maturity minus your basis. If you choose to use the constant yield method to figure accrued acquisition discount, treat the cost of acquiring the obligation as the issue price.

If you choose to use this method, you cannot change your choice. For an obligation listed above that is not a government obligation, the amount you include in your income for the current year is the accrued OID, if any, plus any other accrued interest payable.

If you choose the constant yield method to figure accrued OID, apply it by using the obligation's issue price. Choosing to include accrued acquisition discount instead of OID. You can choose to report accrued acquisition discount defined earlier under Government obligations rather than accrued OID on these short-term obligations. Your choice will apply to the year for which it is made and to all later years and cannot be changed without the consent of the IRS.

You must make your choice by the due date of your return, including extensions, for the first year for which you are making the choice. Attach a statement to your return or amended return indicating: The choice you are making and that it is being made under section c 2 of the Internal Revenue Code;. The period for which the choice is being made and the obligation to which it applies; and. Any other information necessary to show you are entitled to make this choice. Choosing to include accrued discount and other interest in current income. If you acquire short-term discount obligations that are not subject to the rules for current inclusion in income of the accrued discount or other interest, you can choose to have those rules apply.

This choice applies to all short-term obligations you acquire during the year and in all later years. You cannot change this choice without the consent of the IRS. The procedures to use in making this choice are the same as those described for choosing to include acquisition discount instead of OID on nongovernment obligations in current income.

However, you should indicate that you are making the choice under section b 2 of the Internal Revenue Code. Also see the following discussion. If you make the election to report all interest currently as OID, you must use the constant yield method. Generally, you can elect to treat all interest on a debt instrument acquired during the tax year as OID and include it in income currently. For purposes of this election, interest includes stated interest, acquisition discount, OID, de minimis OID, market discount, de minimis market discount, and unstated interest as adjusted by any amortizable bond premium or acquisition premium.

When to report your interest income depends on whether you use the cash method or an accrual method to report income. Most individual taxpayers use the cash method. If you use this method, you generally report your interest income in the year in which you actually or constructively receive it. However, there are special rules for reporting the discount on certain debt instruments. Savings Bonds and Discount on Debt Instruments , earlier. You are not in the business of lending money. The note stated that principal and interest would be due on August 31, You constructively receive income when it is credited to your account or made available to you.

You do not need to have physical possession of it. For example, you are considered to receive interest, dividends, or other earnings on any deposit or account in a bank, savings and loan, or similar financial institution, or interest on life insurance policy dividends left to accumulate, when they are credited to your account and subject to your withdrawal. This is true even if they are not yet entered in your passbook. You constructively receive income on the deposit or account even if you must: Pay a penalty on early withdrawals, unless the interest you are to receive on an early withdrawal or redemption is substantially less than the interest payable at maturity.

If you use an accrual method, you report your interest income when you earn it, whether or not you have received it. Interest is earned over the term of the debt instrument. If, in the previous example, you use an accrual method, you must include the interest in your income as you earn it. You would report the interest as follows: Generally, interest on coupon bonds is taxable in the year the coupon becomes due and payable. It does not matter when you mail the coupon for payment. Generally, you report all your taxable interest income on Form , line 8a; Form A, line 8a; or Form EZ, line 2.

Instead, you must use Form A or Form In addition, you cannot use Form EZ if you must use Form , as described later, or if any of the statements listed under Schedule B Form A or , later, are true.

You are claiming the interest exclusion under the Education Savings Bond Program discussed earlier. You received interest from a seller-financed mortgage, and the buyer used the property as a home. You received, as a nominee, interest that actually belongs to someone else. You received a Form INT for interest on a bond you bought between interest payment dates. You acquired taxable bonds after and choose to reduce interest income from the bonds by any amortizable bond premium discussed in chapter 3 under Bond Premium Amortization. List each payer's name and the amount of interest income received from each payer on line 1.

You cannot use Form A if you must use Form , as described next. You forfeited interest income because of the early withdrawal of a time deposit;. You acquired taxable bonds after , you choose to reduce interest income from the bonds by any amortizable bond premium, and you are deducting the excess of bond premium amortization for the accrual period over the qualified stated interest for the period discussed in chapter 3 under Bond Premium Amortization ; or.

You received tax-exempt interest from private activity bonds issued after August 7, In Part I, line 1, list each payer's name and the amount received from each. Total your tax-exempt interest such as interest or accrued OID on certain state and municipal bonds, including zero coupon municipal bonds reported on Form INT, box 8, and exempt-interest dividends from a mutual fund or other regulated investment company reported on Form DIV, box Add these amounts to any other tax-exempt interest you received.

Report the total on line 8b of Form A or Form Do not add tax-exempt interest in the total on Form EZ, line 2. Do not report interest from an individual retirement arrangement IRA as tax-exempt interest. Your taxable interest income, except for interest from U. Add this amount to any other taxable interest income you received. You must report all your taxable interest income even if you do not receive a Form INT.

Your identifying number may be truncated on any paper Form INT you receive. If you forfeited interest income because of the early withdrawal of a time deposit, the deductible amount will be shown on Form INT in box 2. See Penalty on early withdrawal of savings , later. Generally, add the amount shown in box 3 to any other taxable interest income you received. If part of the amount shown in box 3 was previously included in your interest income, see U.

If you redeemed U. Box 4 of Form INT will contain an amount if you were subject to backup withholding. Box 5 of Form INT shows investment expenses you may be able to deduct as an itemized deduction. Chapter 3 discusses investment expenses. You may be able to take a credit for the amount shown in box 6 unless you deduct this amount on line 8 of Schedule A Form To take the credit, you may have to file Form , Foreign Tax Credit.

For a covered security, if you made an election under section b to include market discount in income as it accrues and you notified your payer of the election, box 10 shows the market discount that accrued on the debt instrument during the year while held by you. Report this amount on your income tax return as directed in the instructions for Form or Form A. For a covered security, box 11 shows the amount of premium amortization for the year, unless you notified the payer in writing in accordance with Regulations section 1.

If an amount is reported in this box, see the instructions for Schedule B Form If an amount is not reported in this box for a covered security acquired at a premium, the payer has reported a net amount of interest in boxes 1, 3, 8, or 9, whichever is applicable. If the amount in this box is greater than the amount of interest paid on the covered security, see Regulations section 1. Include this amount in your total taxable interest income. Your identifying number may be truncated on any paper Form OID you receive.

Add this amount to the OID shown in box 1 and include the result in your total taxable income. If you forfeited interest or principal on the obligation because of an early withdrawal, the deductible amount will be shown in box 3. Box 4 of Form OID will contain an amount if you were subject to backup withholding. Box 9 of Form OID shows investment expenses you may be able to deduct as an itemized deduction. Then follow these steps. Several lines above line 2, enter a subtotal of all interest listed on line 1. Below the subtotal enter "U. Savings Bond Interest Previously Reported" and enter amounts previously reported or interest accrued before you received the bond.

Understanding the Net Investment Income Tax - Old North State Trust

Subtract these amounts from the subtotal and enter the result on line 2. Your parents bought U. The bonds were issued in your name, and the interest on the bonds was reported each year as it accrued. See Choice to report interest each year , earlier. The bond was originally issued in March You received no other taxable interest for You file Form A. If you had other taxable interest income, you would enter it next and then enter a subtotal, as described earlier, before going to the next step.

Several lines above line 2, enter "U. You redeem the bond when it reaches maturity. Below this subtotal, enter "U. You then complete the rest of the form. Worksheet for savings bonds distributed from a retirement or profit-sharing plan. If you cashed a savings bond acquired in a taxable distribution from a retirement or profit-sharing plan as discussed under U.

Savings Bonds , earlier , your interest income does not include the interest accrued before the distribution and taxed as a distribution from the plan. Use the worksheet below to figure the amount you subtract from the interest shown on Form INT. You received a distribution of Series EE U. This is the amount you included on your return. Since a part of the interest was included in your income in , you need to include in your income only the interest that accrued after the bond was distributed to you. On Schedule B Form A or , line 1, include all the interest shown on your Form INT as well as any other taxable interest income you received.

- Judicial Activity Concerning Enemy Combatant Detainees: Major Court Rulings;

- Information Menu;

- Esthétique théâtrale (Lettres) (French Edition).

- Help Menu Mobile;

- Happy Blended Families: How Step Families Can Get Along!

- Publication (), Investment Income and Expenses | Internal Revenue Service.

- Rezepte zum Abnehmen - Die 22 leckersten Fischrezepte mit Tipps zum Abnehmen und schlank bleiben - Fett verbrennen mit gesunder Ernährung (Rezepte zum ... verbrennen mit gesunder 6) (German Edition);

Several lines above line 2, put a subtotal of all interest listed on line 1. Below this subtotal enter "U. Savings Bond Interest Previously Reported" and enter the amount figured on the worksheet below. Use Form to figure your interest exclusion when you redeem qualified savings bonds and pay qualified higher educational expenses during the same year.

For more information on the exclusion and qualified higher educational expenses, see the earlier discussion under Education Savings Bond Program. You must show your total interest from qualified savings bonds you cashed during on Form , line 6, and on Schedule B Form A or If an individual buys his or her home from you in a sale that you finance, you must report the amount of interest received on Schedule B Form A or , line 1.

Include on line 1 the buyer's name, address, and SSN. You must also give your name, address, and SSN or employer identification number to the buyer. Even if you receive a Form INT for interest on deposits that you could not withdraw at the end of , you must exclude these amounts from your gross income. See Interest income on frozen deposits , earlier.

Do not include this income on line 8a of Form A or Several lines above line 2, put a subtotal of all interest income. Below this subtotal, enter "Frozen Deposits" and show the amount of interest that you are excluding. Subtract this amount from the subtotal and enter the result on line 2.

Then, below a subtotal of all interest income listed, enter "Accrued Interest" and the amount of accrued interest you paid to the seller. That amount is taxable to the seller, not you. Subtract that amount from the interest income subtotal. Enter the result on line 2 and also on line 8a of Form A or Then, below a subtotal of all interest income listed, enter "Nominee Distribution" and the amount that actually belongs to someone else.

For more information about the reporting requirements and the penalties for failure to file or furnish certain information returns, see the General Instructions for Certain Information Returns. Because your SSN was given to the bank, you received a Form INT for that includes the interest income earned belonging to your sister. Show your sister's name, address, and SSN in the blocks provided for identification of the "Recipient. Identify the amount as "OID Adjustment" and subtract it from the subtotal.

If you withdraw funds from a certificate of deposit or other deferred interest account before maturity, you may be charged a penalty. The Form INT or similar statement given to you by the financial institution will show the total amount of interest in box 1 and will show the penalty separately in box 2. You must include in income all interest shown in box 1. You can deduct the penalty on Form , line Deduct the entire penalty even if it is more than your interest income. Dividends are distributions of money, stock, or other property paid to you by a corporation or by a mutual fund.

You also may receive dividends through a partnership, an estate, a trust, or an association that is taxed as a corporation. However, some amounts you receive called dividends are actually interest income. See Dividends that are actually interest , earlier. Most distributions are paid in cash check.

Publication 550 (2017), Investment Income and Expenses

However, distributions can consist of more stock, stock rights, other property, or services. Most corporations use Form DIV to show you the distributions you received from them during the year. Keep this form with your records. Your identifying number may be truncated on any paper Form DIV you receive. Even if you do not receive a Form DIV, you must still report all your taxable dividend income.

For example, you may receive distributive shares of dividends from partnerships or S corporations. If someone receives distributions as a nominee for you, that person will give you a Form DIV, which will show distributions received on your behalf. Certain substitute payments in lieu of dividends or tax-exempt interest received by a broker on your behalf must be reported to you on Form MISC, Miscellaneous Income, or a similar statement.

See also Reporting Substitute Payments , later. If you receive a Form that shows an incorrect amount or other incorrect information , you should ask the issuer for a corrected form. The new Form you receive will be marked "Corrected. If stock is sold, exchanged, or otherwise disposed of after a dividend is declared but before it is paid, the owner of record usually the payee shown on the dividend check must include the dividend in income.

If a mutual fund or other regulated investment company or real estate investment trust REIT declares a dividend including any exempt-interest dividend or capital gain distribution in October, November, or December, payable to shareholders of record on a date in one of those months but actually pays the dividend during January of the next calendar year, you are considered to have received the dividend on December You report the dividend in the year it was declared.

Related Items:

Ordinary dividends are the most common type of distribution from a corporation or a mutual fund. They are paid out of earnings and profits and are ordinary income to you. This means they are not capital gains. You can assume that any dividend you receive on common or preferred stock is an ordinary dividend unless the paying corporation or mutual fund tells you otherwise. Ordinary dividends will be shown in box 1a of the Form DIV you receive.

They should be shown in box 1b of the Form DIV you receive. The dividends must have been paid by a U. See Qualified foreign corporation , later. The dividends are not of the type listed later under Dividends that are not qualified dividends. You must have held the stock for more than 60 days during the day period that begins 60 days before the ex-dividend date. The ex-dividend date is the first date following the declaration of a dividend on which the buyer of a stock is not entitled to receive the next dividend payment.

When counting the number of days you held the stock, include the day you disposed of the stock, but not the day you acquired it. See the examples below. In the case of preferred stock, you must have held the stock more than 90 days during the day period that begins 90 days before the ex-dividend date if the dividends are due to periods totaling more than days. If the preferred dividends are due to periods totaling less than days, the holding period in the preceding paragraph applies. You bought 5, shares of XYZ Corp. The ex-dividend date was July 12, However, you sold the 5, shares on August 8, You held your shares of XYZ Corp.

The day period began on May 13, 60 days before the ex-dividend date , and ended on September 10, You have no qualified dividends from XYZ Corp. Assume the same facts as in Example 1 except that you bought the stock on July 11, the day before the ex-dividend date , and you sold the stock on September 13, You held the stock for 63 days from July 12, , through September 13, ABC Mutual Fund paid a cash dividend of 10 cents per share.

The ABC Mutual Fund advises you that the portion of the dividend eligible to be treated as qualified dividends equals 2 cents per share. However, you sold the 10, shares on August 8, Holding period reduced where risk of loss is diminished. When determining whether you met the minimum holding period discussed earlier, you cannot count any day during which you meet any of the following conditions.

You had an option to sell, were under a contractual obligation to sell, or had made and not closed a short sale of substantially identical stock or securities. You were grantor writer of an option to buy substantially identical stock or securities. Your risk of loss is diminished by holding one or more other positions in substantially similar or related property.

For information about how to apply condition 3 , see Regulations section 1. A foreign corporation is a qualified foreign corporation if it meets any of the following conditions. The corporation is eligible for the benefits of a comprehensive income tax treaty with the United States that the Department of the Treasury determines is satisfactory for this purpose and that includes an exchange of information program. For a list of those treaties, see Table The corporation does not meet 1 or 2 above, but the stock for which the dividend is paid is readily tradable on an established securities market in the United States.

See Readily tradable stock , later. A corporation is not a qualified foreign corporation if it is a passive foreign investment company during its tax year in which the dividends are paid or during its previous tax year. Dividends paid out of a CFC's earnings and profits that were not previously taxed are qualified dividends if the CFC is otherwise a qualified foreign corporation and the other requirements in this discussion are met. Certain dividends paid by a CFC that would be treated as a passive foreign investment company but for section d of the Internal Revenue Code may be treated as qualified dividends.

For more information, see Notice , which can be found at www. Any stock or American depositary receipt in respect of that stock is considered to satisfy requirement 3 under Qualified foreign corporation , if it is listed on a national securities exchange that is registered under section 6 of the Securities Exchange Act of or on the Nasdaq Stock Market. For a list of the exchanges that meet these requirements, see www. The following dividends are not qualified dividends. They are not qualified dividends even if they are shown in box 1b of Form DIV.

Dividends paid on deposits with mutual savings banks, cooperative banks, credit unions, U. Report these amounts as interest income. Dividends from a corporation that is a tax-exempt organization or farmer's cooperative during the corporation's tax year in which the dividends were paid or during the corporation's previous tax year.

Dividends paid by a corporation on employer securities held on the date of record by an employee stock ownership plan ESOP maintained by that corporation. Dividends on any share of stock to the extent you are obligated whether under a short sale or otherwise to make related payments for positions in substantially similar or related property. Payments in lieu of dividends, but only if you know or have reason to know the payments are not qualified dividends. Payments shown on Form DIV, box 1b, from a foreign corporation to the extent you know or have reason to know the payments are not qualified dividends.

The corporation in which you own stock may have a dividend reinvestment plan. This plan lets you choose to use your dividends to buy through an agent more shares of stock in the corporation instead of receiving the dividends in cash. Most mutual funds also permit shareholders to automatically reinvest distributions in more shares in the fund, instead of receiving cash.

If you use your dividends to buy more stock at a price equal to its fair market value, you still must report the dividends as income. If you are a member of a dividend reinvestment plan that lets you buy more stock at a price less than its fair market value, you must report as dividend income the fair market value of the additional stock on the dividend payment date. You also must report as dividend income any service charge subtracted from your cash dividends before the dividends are used to buy the additional stock.

But you may be able to deduct the service charge. See Expenses of Producing Income in chapter 3. In some dividend reinvestment plans, you can invest more cash to buy shares of stock at a price less than fair market value. If you choose to do this, you must report as dividend income the difference between the cash you invest and the fair market value of the stock you buy.

When figuring this amount, use the fair market value of the stock on the dividend payment date. Report amounts you receive from money market funds as dividend income. Money market funds are a type of mutual fund and should not be confused with bank money market accounts that pay interest.

Capital gain distributions also called capital gain dividends are paid to you or credited to your account by mutual funds or other regulated investment companies and real estate investment trusts REITs.